Tag Archives: Beneficial Ownership Cayman Islands

On 31 July 2024, the Beneficial Ownership Transparency Act 2023 (the “Act”) came into force in the Cayman Islands which compels every Cayman Islands entity[1] (an “Entity”) to (a) maintain a register of beneficial owners in conjunction with their corporate service providers (b) to review and verify the information provided is accurate and (c) to report details of such beneficial owners to the competent authority[2] on a monthly basis. While these changes are now in force, industry has until 1 January 2025 to comply before enforcement commences[3]. HSM Partner Robert Mack explores how the Cayman Islands Beneficial Ownership regime impacts private wealth structures.

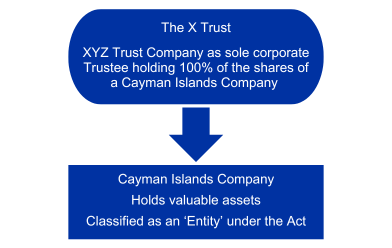

While the previous beneficial ownership regime has been in place since 2017, the recent changes contained in the Act expand the scope to capture a wider range of legal persons, including limited partnerships, exempted limited partnerships, private trust companies and foundation companies. There are also new requirements to describe the nature of the ownership or control of an entity and to confirm the nationality of any beneficial owner. Trusts, however, remain out of scope. That said, it is very common for trust structures to contain at least one Entity to act as a holding vehicle for trust assets. A simple example of such a trust structure appears below:

The Act requires all beneficial owners of an Entity to be identified and reported on a monthly basis via a secure online government portal[4]. In scenarios where a trust structure contains one or more Entities there are four possible outcomes:

- If a trustee owns a minimum of 25% of the shares of an Entity or 25% or more of the voting rights / partnership interests of an Entity such trustee will be classified as a (or the) beneficial owner.

- If a trustee exercises control of an Entity it will be classified as a beneficial owner.

- If an individual, not being the trustee, owns more than 25% of the Entity or 25% or more of the voting rights / partnership interests such individual will be classified as a (or the) beneficial owner.

- If an individual, not being the trustee, exercises control over the Entity by some means, such individual will be classified as a beneficial owner.

Ascertaining the ownership of an Entity should usually be quite straightforward. If the Entity is a company, any shareholder owning 25% or more of the shares of such Entity will be a beneficial owner. For partnerships, any person holding voting rights or partnership interests in excess of the 25% threshold should qualify as a beneficial owner.

Ascertaining which person or persons ‘controls’ an Entity is not always straightforward where a Cayman Islands trust is involved at the top of the structure either. This will require an analysis of the trust instrument itself as well as an examination of the circumstances surrounding the administration of the trust or Entity.

All Cayman Islands trusts fall into three distinct categories for these purposes:

- Trustee controlled. This means all powers contained in the trust instrument are vested in the trustee alone allowing such trustee to exercise shareholder or related powers for any underlying Entities in the structure as they see fit. In such a scenario the trustee should be identified as the beneficial owner of an Entity under the Act[5].

- Trustee fettered. This means some trust powers are reserved to persons other than the trustee. This can be an ‘enforcer’ or a ‘protector’ or some other person, such as the settlor of the trust. In this scenario, such persons may also be classified as beneficial owners of the Entity.

- Trustee usurped. This is where on the face of the trust instrument all of the trust powers are all vested in the trustee, but in practice some other person or persons are actually controlling the administration of the trust from the shadows to include controlling any Entity owned by the trust. Such trusts are sometimes referred to as ‘sham trusts’ and are extremely rare in practice, especially where professional trustees are involved, but there are numerous examples in trust jurisprudence[6]. In this scenario such persons lurking in shadows may in extreme circumstances be classified as a beneficial owner of an Entity.

Trustee Controlled

Assuming the trustee owns 25% or more of an Entity (or in the case of a partnership, 25% or more of the voting rights or partnership rights), it will be classified as a (or the) beneficial owner under the Act and no further analysis is required.

In instances where the trustee owns less than 25% of an Entity (or in the case of a partnership, 25% or more of the voting rights or partnership rights), yet somehow exercises control over an Entity, such trustee should also be classified as a beneficial owner.

Trustee Fettered

Section 14 of the Trusts Act (2021 Revision) allows the settlor of a Cayman Islands trust to reserve a range of key powers to himself or others (“Powerholders”) in the trust instrument. Such powers include powers to:

- Revoke, vary or amend the trusts or powers contained in the trust instrument;

- Appoint income or capital of the trust fund;

- Enable a settlor to reserve a limited beneficial interest in trust property in some manner;

- Act as a director or officer or any company owned by the trust;

- Give binding directions to a trustee concerning the management of trust investments;

- Appoint, add, or remove any trustee, protector or beneficiary;

- Change the governing law and the forum of administration of the trust; and

- Impose consent requirements on the exercise of one or more trustee powers.

An assessment will have to be made on a case-by-case basis whether (or not) one or more of these reserved powers amount to ‘control’ in the hands of a Powerholder for the purposes of the Act. For example, any consent requirements imposed on a trustee over the exercise of their powers would almost certainly amount to ‘control’ according to Regulation 29(3)(c) of the Beneficial Ownership Transparency Regulations (31 July 2024 version).

Trustee Usurped

Highly unlikely to ever occur as it would require a trustee to concede they have relinquished control over the administration of the trust to a non-Powerholder.

In this unlikely scenario, an Entity and the corporate service provider would have to include any such non-Powerholder as a beneficial owner in their reporting.

Foundation Companies

The same concepts applicable to trusts apply equally to foundation companies. Therefore, a careful review of the constitutional documents of the Foundation Company and ownership structure[7] will have to be conducted to ascertain whether there are any Powerholders and, if so, what specific powers are reserved to them. Then a determination will have to be made whether (or not) such reserved powers are sufficient to constitute “ultimate effect control” for the purposes of the Act[8]. Special focus should also be given to the powers reserved to the Supervisor and the Founder.

Private Trust Companies

All private trust companies are in scope under the Act. As such, analysis of the constitutional documents and the ownership structure will now be required. Given that the shares of private trust companies are typically held in private purpose trusts / STAR trusts, the terms of such private purpose trusts / STAR trusts and the conduct of their administration will require careful analysis.

Summary

The steps and time required to accurately comply with the recent changes to the Cayman Islands beneficial ownership regime should not be underestimated especially in light of the looming enforcement deadline of 1 January 2025 (just over eight weeks from the date of this article) and given the consequences for non-compliance can be dire[9].

Trustees should identify any relevant Entities in their trust structures, and then complete the analysis of their trust instruments and surrounding circumstances to ensure their reporting is accurate and complete at the Entity level.

Directors of foundation companies and private trust companies should also conduct a similar exercise with respect to their constitutional documents and ownership structure to include an examination of circumstances surrounding the conduct of the administration of these Entities to ensure accurate reporting.

HSM’s team can assist with the necessary review and coordination of requirements to ensure accurate reporting is accomplished.

Footnotes

[1] Entities include companies, foundation companies, limited liability partnerships, limited partnerships, exempted limited partnerships, private trust companies, and other legal persons as may be prescribed in relevant regulations (none are specified at this moment in time). Trusts are not classified as Entities under the Act.

[2] The competent authority in this case is the Minister of Financial Services, who has delegated this function to the Cayman Islands General Registry.

[3] One change for example appears in Section 8 of the Act requires (subject to certain exemptions) persons who have been identified as beneficial owners to be given notice in writing, and such beneficial owners have a 30-day window to agree (or otherwise) their status as a beneficial owner and to confirm or correct their particulars. This 30-day window will have to be factored into the 1 January 2025 enforcement deadline.

[4] The information stored on this portal is not currently publicly accessible.

[5] This is separate and distinct from usual trust principles. An orthodox trust arrangement requires the trustee to hold legal title to trust property for the benefit of its beneficiaries, and it is the beneficiaries who are considered to be the collective beneficial owners as a matter of equity.

[6] See Rahman v Chase Bank (CI) Trust Co. Ltd [1991] JLR for a particularly stark example.

[7] Most foundation companies are structed as limited by guarantee companies and do not have shares or shareholders. As a result, thought will have to be given as to whether the guarantee members qualify as beneficial owners.

[8] ‘Ultimate Effective Control’ is defined in the Act to include ownership and control exercised through a chain of ownership or (rather cryptically) by means of control other than direct control.

[9] CI$5,000 per breach, with a rolling penalty of CI$1,000 for each month the breach remains unremedied. There is also scope for fines of up to CI$100,000 for repeatedly failing to comply with certain obligations arising under the Act. Non-compliance can also result in an Entity being struck from the Register. There are also possible custodial sentences up to two years for mangers, directors, members or other officers of any non-complaint Entity in certain circumstances.

Further to the publication of the Beneficial Ownership Transparency Act, 2023, which came into force on 31 July 2024, the Cayman Islands Government is seeking comments on draft Beneficial Ownership Transparency (Legitimate Interest Access) Regulations, 2024 (the “LIA Regulations”) and draft Beneficial Ownership Transparency (Access Restriction) Regulations, 2024 (the “Access Restriction Regulations”). Once finalised, the new regulations, will allow members of the public to apply for beneficial ownership information subject, however, to legitimate interest requirements and/or restrictions in certain circumstances.

As anticipated, the LIA Regulations set out the framework for members of the public, who can evidence a legitimate interest, access to beneficial ownership information for a specific legal person, subject to a two part test.

A member of the public (the “Applicant”) may apply for access to information in relation to a legal person on the basis that the Applicant is:

- a person engaged in journalism or bona fide academic research;

- acting on behalf of a civil society organisation whose purpose includes the prevention or combating of money-laundering, its predicate offences or terrorism financing; or

- seeking information in the context of a potential or actual business relationship or transaction with the legal person about whom the information is sought,

and has a legitimate interest in the information sought for the purpose of preventing, detecting, investigating, combating or prosecuting money laundering or its predicate offences or terrorist financing.

The Access Restriction Regulations allow individuals to apply to the competent authority for protection from public disclosure under the LIA Regulations for periods of 3 years where they believe that their association with the legal person, if disclosed, will place them, or an individual living with them, at serious risk of kidnapping, extortion, violence, intimidation, or other similar danger or serious harm.

Conclusion

The draft regulations show the Cayman Islands continued commitment to transparency and anti-money laundering initiatives while remaining in line with international standards and best practices and providing safeguards for the protection of individual privacy in warranted circumstances.

With the Cayman Islands’ continued focus on quality, innovation and expertise, it seems reasonable to expect that the changes brought about by the Regulations will be absorbed by the market and in no way hinder the Cayman Islands’ continued success.

HSM can assist with all beneficial ownership matters and provide the necessary advice as to the application of the new beneficial ownership regime. Please connect with HSM Partner, Christian Victory or HSM Managing Partner, Huw Moses, for any enquiries.

The HSM Group specialises in Corporate and Commercial Law, Litigation, Restructuring, Insolvency, Private Client, Immigration, Employment Law, Family Law, Property, Debt Solutions and Intellectual Property in addition to providing comprehensive corporate services through HSM Corporate Services Ltd.

This publication is intended only to provide a summary of the subject matter covered. It does not purport to be comprehensive or to provide legal advice. No person should act in reliance on any statement contained in this publication without first obtaining specific professional advice. Alternative solutions also exist which may better suit the requirements of a particular individual or entity.

Fatal error: Uncaught Error: Call to undefined function twentythirteen_paging_nav() in /home/clients/d17af2243e6f179e393695ba6e9ce04e/hsmnew/wp-content/themes/hsm/tag.php:33 Stack trace: #0 /home/clients/d17af2243e6f179e393695ba6e9ce04e/hsmnew/wp-includes/template-loader.php(78): include() #1 /home/clients/d17af2243e6f179e393695ba6e9ce04e/hsmnew/wp-blog-header.php(19): require_once('/home/clients/d...') #2 /home/clients/d17af2243e6f179e393695ba6e9ce04e/hsmnew/index.php(17): require('/home/clients/d...') #3 {main} thrown in /home/clients/d17af2243e6f179e393695ba6e9ce04e/hsmnew/wp-content/themes/hsm/tag.php on line 33