Tag Archives: Cayman Islands Law

Through the International Tax-Co-operation (Economic Substance) Law, 2018, the concept of an Economic Substance Test has been introduced and certain businesses must satisfy new requirements. The test applies to any “in scope” businesses and requires that any “relevant entity” carrying on a “relevant activity” must pass a 3 pronged test. Download our client guide to determine if your business is within scope or continue reading below.

Economic Substance Test

Certain categories of business operating from within the Cayman Islands must be in a position to demonstrate that, relative to the size and nature of their operations, they have sufficient “economic substance”. Such substance is measured in terms of a demonstrable physical presence, including of the mind, management and control of a relevant organisation.

If you are a relevant entity carrying on a relevant activity – you must:

(a) conduct Cayman Islands core income generating activities in relation to that relevant activity

(b) be directed and managed in an appropriate manner in the Islands in relation to that relevant activity; and

(c) having regard to the level of relevant income derived from the relevant activity carried out in the islands –

a. have an adequate amount of operating expenditure incurred in the islands;

b. have an adequate physical presence (including maintaining a place of business or plant, property and equipment) in the Islands; and

c. have an adequate number of full time employees or other personnel with appropriate qualifications in the Islands.

Definitions

A relevant entity is:

1. A company (other than a domestic company) that is-

a) incorporated under the Companies Law (as Revised) or

b) an LLC registered under the Limited Liability Companies Law (as Revised).

2. A Limited Liability Partnership that is registered under in accordance with the Limited Liability Partnership Law (as Revised)

3. A foreign company registered in the Cayman Islands under part IX of the Companies Law (as Revised)

Investment Funds or entities which are tax resident outside of the Islands are not considered relevant entities.

An “Investment Fund” is defined as an entity whose principal business is the issuing of investment interests to raise funds or pool investor funds with the aim of enabling a holder of such an investment interest to benefit from the profits or gains from the entity’s acquisition, holding, management or disposal of investments and includes any entity through which an investment fund directly or indirectly invests or operates.

A domestic company is a company that is not part of an MNE Group that is:

1. Carrying on business in the islands and which complies with s.4(1) of the Local Companies Control Law (as Revised) i.e. is Caymanian owned and controlled (at least 60% of the board of directors is comprised of Caymanians and at least 60% of the issues shares are held in the names of Caymanians) or holds a valid Trade and Business Licence under the Trade and Business Licensing Law (as Revised), is licensed under the Banks & Trust Companies Law (as Revised) or is otherwise operating under a franchise granted by the Cayman Islands Government.

2. A Company Limited by Guarantee or an “Association not for Profit” under s.80 of the Companies Law (as Revised).

Or a subsidiary of such company.

An MNE Group is a Group with annual revenues of at least US$850m total consolidated group revenue.

“Group” means a collective of two or more enterprises that are tax resident in different jurisdictions and are related through ownership or control such that it is (or would be traded on a public securities exchange) required to prepare Consolidated Financial Statements for financial reporting purposes.

A relevant entity is in scope if it is carrying on one or more of the below relevant activities:

a) Banking business;

i.e. the business of receiving (other than from a bank or trust company) and holding on current, savings, deposit or other similar account money which is repayable by cheque or order and may be invested by way of advances to customers or otherwise.

b) Distribution and service centre business;

i.e. the business of either or both of the following –

a) purchasing from an entity in the same Group

i) component parts or materials for goods; or

ii) goods ready for sale, and reselling such component parts, materials or goods outside the islands

b) providing services to an entity in the same Group in connection with the business outside of the Islands

but does not include any activity included in any other relevant activity except holding company business. For the avoidance of doubt, b) above only falls within the definition in the specific circumstances where the relevant entity is operating as a service centre for entities in the same Group.

c) Financing and leasing business;

i.e. the business of providing credit facilities for any kind of consideration to another person but does not include financial leasing of land or an interest in land, banking business, fund management business or insurance business.

d) Fund management business;

i.e. the business of managing securities as set out in paragraph 3 of Schedule 2 to the Securities Investment Business law (2019 Revision) carried on by a relevant entity licensed or otherwise authorised to conduct business under that Law for an investment fund.

e) Headquarters business;

i.e. the business of providing any of the following services to an entity in the same Group –

a) the provision of senior management;

b) the assumption or control of material risk for activities carried out by any of those entities in the same Group; or

c) the provision of substantive advice in connection with the assumption or control of risk referred to in paragraph b)

but does not include banking business, financing and leasing business, fund management business, intellectual property business, holding company business or insurance business.

f) Holding company business;

i.e. the business of a ‘pure equity holding company’, which itself is defined to mean ‘a company that only holds equity participations in other entities and only earns dividends and capital gains’.

g) Insurance business;

i.e. the business of accepting risks by effecting or carrying out contracts of insurance, whether directly or indirectly, and includes running-off business including the settlement of claims.

h) Intellectual property business; or

i.e. the business of holding, exploiting or receiving income from intellectual property assets and ‘intellectual property asset’ means an intellectual property right including a copyright, design right, patent and trade mark.

i) Shipping business

Means any of the following activities involving the operation of a ship anywhere in the world other that in the territorial waters of the Islands or between the Islands –

a) the business of transporting, by sea passengers or animals, goods or mail for a charge;

b) the renting or chartering of ships for the purpose describe in paragraph a);

c) the sale of travel tickets and ancillary ticket related services connected with the operation of a ship;

d) the use, maintenance or rental of containers, including trailers and other vehicles or equipment for the transport of containers, used for the transport of anything by sea; or

e) the functioning as a private seafarer recruitment and placement service

but does not include a holding company business or the owning, operating or chartering of a pleasure yacht.

Given the above, the test can be substantially satisfied through the employment of persons within the Islands to carry out the relevant activity or activities. The Cayman Islands may already have persons with the requisite skills and expertise already resident, but where such skills are unavailable, or if available, are not available in sufficient number, then any required persons can be brought into the Islands from overseas. Such persons can bring with their spouses and children (amongst others) following a well-established immigration regime overseen by a Cayman Islands Government Department, “Workforce Opportunity and Residence Cayman” (WORC).

Compliance, Filings and Penalties

Relevant Entities in existence prior to 1 January 2019 must satisfy the economic substance test in relation to a Relevant Activity from 1 July 2019. Relevant Entities formed on or after 1 January 2019 must satisfy the economic substance test in relation to a Relevant Activity from the date on which the Relevant Entity commences the Relevant Activity.

Starting in 2020 all Relevant Entities carrying Relevant Activities are required to satisfy the economic substance test and submit details to the Cayman Islands Tax Information Authority (the “TIA”). Failure to comply can result in an initial fine of CI$10,000 which can increase to CI$100,000 with continued failure to comply and being struck from the Registrar of Companies.

Next Steps

If you are affected by this Law or if you are unsure, contact our team for tailored advice. We can help determine whether a client is “in scope” or “out of scope” in relation to the economic substance test and if affected, provide administrative support as well as provide immigration advice to issues that may arise.

In order for a Cayman Islands Will to be valid it must be both ‘essentially’ valid and ‘formally’ valid. HSM’s Head of Private Client and Trusts, Robert Mack, explores this structure and what’s new for 2019.

Essential Validity

For a Cayman Islands Will to be ‘essentially’ valid, the person creating it must possess the fundamental power derived from the law of their domicile1 to dispose of their property by Will. Persons who are suffering from a loss or a diminishment of mental capacity for example would typically, under most legal systems, be incapable of disposing of the property by Will or otherwise until such time (if any) as they regain a sufficient degree of their mental faculties.

Legal systems themselves can sometimes impose restrictions on its citizens concerning the disposal of property on death. This typically occurs in ‘civil’ law jurisdictions in Europe and Latin America, Islamic law-influenced jurisdictions, and in some common law jurisdictions,2 where such legal systems prescribe that a deceased person’s property or a portion a deceased person’s property must pass to certain people in certain prescribed shares. Typically those people are comprised of spouses3, children, and other close blood relations of the deceased.

In relation to real/immovable property, it is usual that the legal system of the country where the real/immovable property is situated will be the legal system which governs how such real property will pass on the death4. Therefore, any attempts to use a Cayman Islands Will to control the devolution of foreign5 real property may fail if the succession regime of the foreign country differs from that of the Cayman Islands. In such circumstances it is usually preferable to have a separate Will (if possible/permissible) governed by the law of the country in which the real property is located and to take advice from local attorney in that country regarding the local laws and procedures governing the devolution of real property on death.

The Cayman Islands, in contrast to many other legal systems in the world, offers complete freedom of testamentary disposition, meaning that so long as the Will is ‘essentially’ valid and ‘formally’ valid (see more below), a testator or testatrix may dispose of his or her own property6 as they see fit, and it is extremely difficult for disappointed heirs to challenge an otherwise valid Cayman Islands Will.

Formal Validity

Formal validity refers to the legal formalities which must be observed in order to perfect an ‘essentially’ valid Will. For a Will to be formally valid in the Cayman Islands, it must be (1) in writing, (2) signed at the foot of the Will by the testator or testatrix and (3) be witnessed by two witnesses who must be present at the moment the Will is signed by the testator or testatrix and must attest as such by way of signature on the Will.

If any one of the above three elements are missing, the Will cannot be formally valid as a matter of Cayman Islands law, even if the Will is essentially valid.

So what’s new?

On 1st February 2019, The Formal Validity of Wills (Persons Dying Abroad) Law, 2018 (the “Law”)7 came into force. The Law seeks to simplify the formal validity process by allowing Cayman Islands governed Wills, which are executed by foreign domiciled individuals, from being declared invalid on the grounds that they fail to satisfy the formal validity procedures prescribed by the testators or testatrix’s place of domicile.

The Law states that so long as the Cayman Islands requirements for formal validity are satisfied, the Will should not be declared invalid simply because the testator or testatrix failed to observe the formal validity requirements imposed by the legal system of their place of domicile8.

So for example, if a testator is domiciled in a jurisdiction which requires that Wills must be executed in the presence of a Notary Public and that does not in fact happen, so long as the Will is expressed to be governed by Cayman Islands law and it conforms to the Cayman Islands formal validity requirements, it will be considered valid as a matter of Cayman Islands law.

It’s important to note that the Law doesn’t attempt to modify the requirements for the ‘essential’ validity of a Will.

Why is this important?

Given the Cayman Islands is a magnet for international investment and asset structuring, many people from around the world routinely own valuable assets in the Cayman Islands and often utilise Cayman Islands holding companies to hold such valuable assets. As such, the well-advised client is usually encouraged to put a Cayman Islands Will in place to govern how their Cayman Islands property, including shares in a Cayman Islands company, should devolve upon death. Before the Law came into force, simply adhering to the Cayman Islands test for formal validity might not be sufficient to guarantee the validity of a Cayman Islands Will where a foreign domiciled testator or testatrix was involved — a critical point which is sometimes overlooked.

In a nutshell, the Law provides a safety net in such circumstances to make an otherwise formally invalid Will valid, so long as the Cayman Islands requirements regarding formal validity are observed.

Helpfully, the Law is drafted such that it covers Wills made prior to the introduction of the Law, so it appears to have retrospective effect. This is great news for all of the Cayman Islands Wills floating around the four corners of the Earth, as the Law increases the chances of Wills made prior to the 1st of February 2019 being considered formally valid as a matter of Cayman Islands law even if prior to the 1st of February 2019 they may have been formally invalid.

Conclusion

The Law has improved the odds that Cayman Islands Wills for international clients whether past, present or future will be found to be formally valid as a matter of Cayman Islands law, regardless of any contradictory laws, policies, or procedures which may exist in other parts of the world. This will certainly provide an extra layer of comfort and protection for international clients who utilise or have utilised the Cayman Islands as a planning and structuring base.

This article can also be seen on Mondaq – March 2019.

Footnotes

1 The method of establishing a persons’ domicile is outside of the scope of this article, however, it can be quite complex and requires a careful examination of the personal history of the testator or testatrix.

2 England, for example, has in place The Inheritance (Provision for Family and Dependants) Act 1975, which allows persons closely connected with a deceased testator or testatrix, such as a child or spouse/civil partner, or other dependants to make a claim for financial provision against an estate even where the Will is otherwise valid if such aggrieved individual believes they are entitled to a share or a greater share of the estate by reason of a close relationship with the deceased.

3 Often civil or common law partners are included in this definition.

4 Section 5(1)(b) of the Law specifically states that in relation to foreign real property, the execution formalities regarding the devolution of such real property must conform with the laws of such foreign territory rather than those of the Cayman Islands.

5 Meaning outside of the Cayman Islands.

6 Assuming the property is unencumbered, and is not jointly owned for example.

7 Despite the name of the Law, the Law is meant to cover persons who are not domiciled in the Cayman Islands at the time of their death. A person may be domiciled in the Cayman Islands and yet die abroad, but the Law is not intended to address that situation.

8 Section 4(1)(a) of the Law.

Both the same, right? Under the Immigration Law of the Cayman Islands, seemingly not. Unexpected twists and pitfalls await the unwary.

Through decades of tweaking we now find ourselves in a position whereby there are (by our estimation) eight types of Permanent Residence in these Islands (not including The Right to be Caymanian which carries with it many of the fundamental attributes of Permanent Residence, or the various persons granted permission to remain by the Cabinet).

First is that which has been headline-grabbing in recent years, Permanent Residence on the basis of the now (in)famous points system.

Then there is that available to the spouses of such persons (as a Dependant).

Then there is that available to the spouses of Permanent Residents who have applied, on the basis of marriage, for their own Residency and Employment Rights Certificate on the basis of Marriage.

Then there is that available to the children of Permanent Residents following their reaching the age of 18.

Then there is that available to wealthy investors.

Then there is that available to their spouses.

Then (since 13 August 2018) there is that available to the spouses of Caymanians.

The above are all available in consequence of applications made to Workforce, Opportunities and Residence Cayman (“WORC”) under the Immigration (Transition) Law. Each has differing attributes and requirements. Some require annual fees and Annual Declarations, others do not. Some require investment in real estate (and for it to be maintained), others do not. Some restrict the right to work, others prohibit it, and others do not.

Notwithstanding complications and occasional confusion arising from the sheer variety available, the system fundamentally works. Those holding the various types of Permanent Residence outlined above do have one thing in common. They are all able to present their passports to the Immigration Authorities and to receive within it a stamp confirming that the holder of the passport is a Permanent Resident of the Cayman Islands (with or without the Right to Work).

Lastly, there is Permanent Residence available to persons who are Registered as BOTC’s by Registration by Entitlement under the British Nationality Act. Registration by Entitlement is in consequence an application made to the Deputy Governor’s Office that can be made by (or on behalf of) any child who was born in the Cayman Islands and remains a resident until their 10th birthday. These applications do not arise under Cayman Islands domestic legislation. There is no basis to deny such an application, if made by a qualified applicant. There is no need for either parent of the child to be Caymanian, a Permanent Resident, or a BOTC. Simple birth and residence here for the first 10 years of an applicant’s life (together with completing a form, supplying supporting documents, and paying relatively nominal fees) is all that is required.

Our Immigration (Transition) Law (like the Immigration Law before it) clearly confirms that these children have “the Right to remain Permanently in the Islands.” Nevertheless, any attempt by them to obtain a stamp in their passport confirming their right to remain has in our experience been refused. The Authorities contend that the Right to Remain and the Right to Reside are different things. This has been the case for some years and no solution seems imminent. Meanwhile the number of children eligible for confirmation of their “Right to Remain” immigration status in their passports continues to grow.

Those studying our laws governing residence and immigration will note that (appropriately, if they are to have its desired effect of allowing the People of the Cayman Islands to manage the growth of the Permanent Population of these Islands) Term Limits are set at 9 years. Nevertheless, due to numerous loopholes and delays there is no shortage of children who were born here and are still here on their 10th birthday. Their right to Permanent Residence (however described) is appropriate and enshrined within our own Law.

If only they could be given a stamp in their passport, then they could confirm their status in these Islands and freely demonstrate it.

This article can also be seen in The Journal – March 2019 issue.

The HSM Group congratulates Partner William (Bill) Helfrecht for his recognition by Chambers and Partners. For the second consecutive year, William is featured in the Band 3 ranking in the 2019 Chambers Global Guide for dispute resolution: trusts in the Cayman Islands.

William’s practice primarily focuses on advising and acting for liquidators, professional trustees, trust protectors and high net-worth individuals in relation to non-contentious and contentious trust matters, professional negligence and other tort actions, Company Law matters (including directors’ liability and shareholders’ rights) and all forms of disputes concerning the ownership and occupation of land.

A peer who was contacted by Chambers and Partners says: “Bill Helfrecht of HSM Chambers is a highly appreciated practitioner whose practice has a particular focus on trust disputes. He garners respect in the market for his wealth of experience in this field.”

Chambers and Partners is a prestigious hub for lawyer recommendations. They diligently research and feature the world’s best lawyers and have done so since 1990, covering over 185 jurisdictions.

Key Contact:

William Helfrecht – Partner

whelfrecht@hsmoffice.com

Tel: +1 345 815 7418

The HSM Group is thrilled to welcome Associate Shula Sbarro. Shula will be assisting HSM’s Debt Solutions practice, acting for banks, strata corporations and other leading businesses.

Shula joins HSM with over eight years of experience in the legal field with a background in commercial and civil litigation. These matters included mortgage possessions, orders for sale, warrant applications, charging orders, redeterminations, third party debt orders, orders for questioning, return of goods and money claims, summary judgment applications and more.

“Shula’s wide-range of litigation experience will undoubtedly be an asset to our clients, who are seeking solutions in respect of debt recovery. We are proud to have her be part of the team,” shares Huw Moses, Managing Partner at HSM.

Shula is a qualified lawyer in the Cayman Islands and was admitted to the Cayman Islands Bar on March 5, 2019.

HSM’s Immigration team explores the immigration issues that exist in the Cayman Islands between Caymanians and British Overseas Territory (BOT) Citizens.

Passports seem to have originated as a document authorising persons to pass through “the gate” of a medieval city. Times have moved on and (at least according to Wikipedia) passports today are a “travel document usually issued by a country’s government that certifies the identity and nationality of its holder primarily for the purpose of international travel.”

Great in principle, but not accurate in the Cayman context.

Cayman Islands passports are neither issued by the Cayman Islands government, nor do they (usually) confirm the nationality of the holder. They are travel documents certifying the identity of the holder and are used for international travel. Everyone lawfully issued a “Cayman Islands Passport” is a British Overseas Territories Citizen by virtue of a connection with the Cayman Islands.

They may or may not however be Caymanian, and unless the immigration authorities place a stamp in it confirming the bearer to be a Caymanian, the passport itself is not determinative of whether or not the holder is Caymanian. Even persons who hold Cayman Islands passports and were born and have always lived in the Cayman Islands may not be Caymanian.

Even more confusingly, many British Overseas Territories Citizens by virtue of a connection with the Cayman Islands have no inherent right to live and work in (or even enter) the Cayman Islands, even if they have been British Overseas Territories Citizens (automatically) from birth. These will include children born in the Cayman Islands today to parents who hold Permanent Residence (whether or not they are also themselves British Overseas Territories Citizens).

According to the Cayman Islands Immigration Law, the only time a British Overseas Territories Citizen has any inherent right to live in the Cayman Islands by virtue only of their passport is if they became a British Overseas Territories Citizen by registration by entitlement under the British Nationality Act.

Such persons are persons who were born without British Overseas Territories Citizenship in the Islands and, having lived here for the first 10 years of their life, then apply for such registration or, if born in the Islands, have a parent who subsequently becomes settled. Even then, if they work without a work permit, or move away for five years, their right to reside is lost.

Non-Caymanians who are born British Overseas Territories Citizens (i.e. can hold Cayman Islands Passports without having to apply for Registration by Entitlement under the British Nationality Act) have no inherent right to reside or work in the Cayman Islands.

All of this creates an enormous conundrum for all manner of Departments of the Cayman Islands Government. There does not appear to be any uniform or consistently applied mechanism for distinguishing Caymanians from non-Caymanians and (particularly since having a Cayman Islands Passport and being born in the Cayman Islands are often irrelevant considerations to the question of whether or not someone is qualified to (for example) register to vote or obtain a stamp duty waiver as a first time buyer), the risk of arbitrary (and incorrect) determinations is significant.

The Immigration Regulations provide that the holders of Cayman Islands Passports need not fill in landing cards. It is ironic that Caymanians not travelling on a Cayman Islands Passport (many Caymanians do not have one, and some may not even be entitled to obtain one) have to complete landing cards whilst hundreds (or even thousands) of non-Caymanians with Cayman Islands Passports are exempt.

A Gordian Blade is available to the authorities to resolve this longstanding issue through minor changes to the Immigration regime. All that seems required is the will to wield it.

This article can also be seen in The Journal – February 2019 issue.

The HSM Group is proud to sponsor the 2nd Annual Society of Trust and Estate Practitioners (STEP) Cayman Conference, taking place at Kimpton Seafire Resort + Spa in Grand Cayman from January 31 – February 1.

Visit our booth during the conference to learn more about our legal and corporate services, and be entered to win one of our 5-in-1 BBQ tools – a useful memento to remind you of our law firm in the Cayman Islands.

Robert Mack, HSM’s Head of Private Client and Trusts, will be speaking during one of the breakout panel sessions on February 1 at 12pm and will be exploring wealth structuring for PEPs (politically exposed persons) – the impact of politics, conflict and sanctions on PEPs.

Since 2010, Robert has been a council member of the local branch of STEP, where he currently holds the position of Vice Secretary.

Robert also sits on the STEP legislative review sub-committee and the Global Transparency sub-committee, which works in partnership with the Cayman Islands Government to implement and improve legislation connected to the trusts and private client industry. Robert is also the Cayman Islands representative of the STEP Mental Capacity Special Interest Group.

We look forward to connecting with you at this conference.

(L-R): Samantha Bartley and Robert Mack

Several charities in the Cayman Islands have received secondhand office furniture provided by local law firm HSM.

The Family Resource Centre recently moved to a new location in George Town and were thrilled to receive a full desk set complete with joining desks, a filing cabinet and bookshelf.

One Dog at a Time collected two large filing cabinets, which volunteer Paula Wythe says is ideal for storing away pet products such as shampoos, brushes, medications and more.

The Frances Bodden Children’s Home selected a large desk for their facility in West Bay.

This is not the first time HSM has donated office furniture. A few years ago, HSM donated desks to Her Majesty’s Northward Prison for their F-wing, an enhanced living space for selected inmates.

“We are always looking for opportunities to support our community and what better way to start the New Year than helping these charities improve their daily operations,” shares HSM Managing Partner, Huw Moses OBE.

HSM still has desks, cabinets, keyboards, blinds and commercial UPS switches available to a worthy home. Email Alyson Hay at ahay@hsmoffice.com to register your charity for these items.

Photo R-L: Huw Moses (HSM Managing Partner) overseas the departure of this furniture set to Racquel Duhaney (Programme Facilitator at the Family Resource Centre).

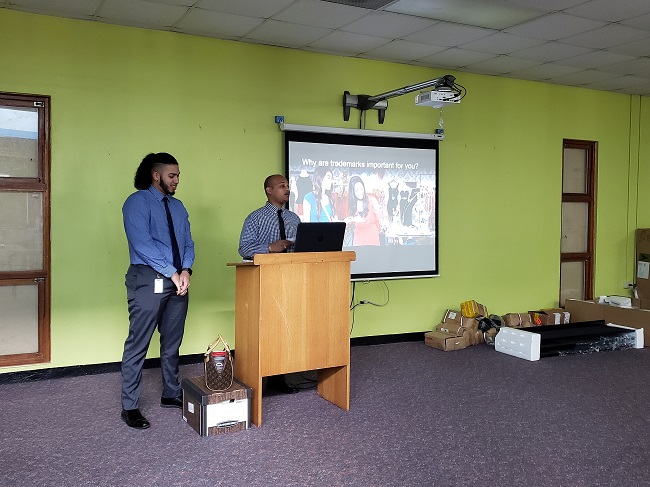

Corey Neysmith and Gabriel Morla of HSM IP Ltd. presented International Trademark Association’s (INTA) Unreal Campaign to over 40 students at the Cayman Islands Further Education Centre (CIFEC) on Thursday, 29 November 2018.

INTA’s Unreal Campaign is a consumer awareness programme aimed at educating teenagers about the importance of trade marks, intellectual property and the dangers of counterfeit products.

Corey, a Senior IP Assistant, started the presentation by explaining the role and importance of registering a trade mark. Corey explains, “A trade mark can be a word, design, service mark and can even be the shape of a building. If a company doesn’t register their distinct features, then a competitor can rightfully take ownership of their ideas and with it, their customer base.”

Since 1 August 2017, it has become possible to register a trade mark in the Cayman Islands without having to go through the United Kingdom or European Union first, thanks to the implementation of The Trade Marks Law, 2016.

Gabriel, an IP Assistant and past CIFEC student, delivered the second part of the presentation which focused on counterfeiting. Gabriel shares, “We stressed the economic impact created when people purchase knockoffs. Counterfeits not only pose a threat to your health and safety, but they directly hurt businesses in the form of job losses and their reputation.”

The students then enjoyed a game of “spot a fake”, where they had to guess between two similar looking products and identify the reasons as to why one of them was the fake. Afterwards, there was a lively discussion for Q&A.

This is the fourth time that HSM IP has presented to students in the Cayman Islands as part of the Unreal Campaign initiative and encourages all consumers to be vigilant when shopping.

Studies show that counterfeiting is rising at an alarming rate. It is estimated that by 2022, the global total value of counterfeit goods could reach US $2.8 trillion, according to a 2017 impact study, The Economic Impacts of Counterfeiting and Piracy, released by Frontier Economics and commissioned by INTA and the International Chamber of Commerce’s Business Action to Stop Counterfeiting and Piracy.

“It is rewarding for our team to be able to share their expertise with our local community and to bring awareness of the negative impacts caused by purchasing counterfeit products,” shares HSM IP Managing Partner, Huw Moses. “Consumers of all ages need to be alert to the risks of purchasing counterfeits, which may expose them not just to financial loss but physical harm.”

Gabriel Morla (left) and Corey Neysmith (right) Share the Importance of Trade Marks

Our Head of Private Client and Trusts, Robert Mack, takes a look at Foundation Companies in the Cayman Islands and how they differ to trusts in the private client context.

In late 2017, Foundation Companies in the Cayman Islands were unveiled to the world. The Foundation Company (“FC”) was designed to act as a corporate wealth and succession planning vehicle; in some cases, it could be a viable alternative to a trust.

There are also new and unexpected uses for FCs, such as acting as a platform for emerging cryptocurrencies and special purpose vehicles in commercial transactions.

The first thing to understand about FCs is that they are merely a variant of a Cayman Islands company and are distinct in nature from civil law foundations found in places such as Panama, Lichtenstein, and certain offshore financial centers such as Jersey. FCs also have a separate legal personality, directors, officers, plus a registered office. So what sets them apart from other Cayman Islands companies? A few key distinctions are as follows:

- FCs are not designed to distribute profits to members, but rather they are meant to carry out particular purposes in accordance with its constitution. In the trust-substitute context, a key purpose is usually to hold valuable assets in order to provide a financial benefit to a defined class of beneficiaries;

- FCs do not have to issue shares, and can, therefore, be ownerless or ‘orphan’ vehicles;

- The purposes of an FC can be entrenched, so no person or court can alter them unless the founder of the FC permits it.

It is also important to understand just how FCs differ from trusts:

- Trusts do not have a separate legal personality. The term ‘trust’ merely describes the relationship which arises when assets/property are held by one person (i.e., a trustee) for the benefit of other persons or purposes (i.e., beneficial objects);

- Trustees are the legal owners of the trust assets;

- The terms of a trust can, in certain circumstances, be changed without the consent or approval of the settlor;

- Unless a Cayman Islands trust is a private purpose or charitable trust, it has a maximum duration of 150 years; FC’s, on the other hand, are perpetual;

- The courts of the Cayman Islands have broader scope to interfere in the administration of trusts than FCs.

Perhaps the biggest ‘leap of faith’ any person wishing to set up a trust must face is the fact that once they part with their valuable assets, it is the trustee who becomes the legal owner of those assets and it is the trustee who makes all the decisions about the management of those assets going forward[1]. This loss of control, while often beneficial from a planning perspective, is often a step too far for some clients, even though it is possible for a settlor of a Cayman Islands trust to reserve to himself or others, certain key administrative powers such as a power to control distributions of capital and income[2].

On the other hand, FCs allow a client to achieve effective control over the FC assets, whether directly (i.e., by taking up a role as a director or officer of the FC), or indirectly (i.e., by appointing trusted individuals as directors or officers of the FC).

While the vast majority of settlors will appoint a professional trustee to administer their trusts[3], an FC may be staffed by the client, family members, or trusted advisors[4]. This could result in minimising administrative expenses if professional directors and officers are not involved[5]. In contrast, for example, private purpose trusts (known as STAR trusts in the Cayman Islands) require that at least one of the trustees is a regulated Cayman Islands trust corporation, and such professional trustee will look to charge market rate for their services.

Foundation Companies in the Cayman Islands offers clients a new and exciting way for clients to structure their affairs with a more familiar corporate entity, and in addition the FC enables clients to be as hand-on or hands-off on the administration of the FC as they wish to be without the risk of tainting the structure[6]. For the client wary of trusts, the FC is an excellent alternative and worthy of consideration.

Cayman Financial Review

This article can also be seen in Cayman Financial Review – Q4 2018 issue.

Footnotes

[1] Subject to the terms of the trust instrument and the law generally. It is possible in some circumstances for a client to act as the trustee of his or her own trust, however, that is often inadvisable for a whole range of reasons which are outside of the scope of this article.

[2] Often times it is impractical or inadvisable for a Settlor to reserve such powers as it may have an adverse tax consequence in his or her place of tax residence.

[3] Due to the complexity of trust administration, tax efficiency, and Cayman Islands legislation which prescribe that professional trustees must appointed for certain types of trusts (ie. STAR trusts).

[4] The only requirement is that the Secretary of an FC must be a ‘qualified person’ being a person who is licensed to provide company management services in the Cayman Islands.

[5] An annual government maintenance fee of approximately US$853 is payable for each year the FC is registered however. Trusts to not attract any such annual fees.

[6] If too many trustee powers are usurped, or if the trustee/settlor relationship becomes corrupted there is a risk the trust may be deemed to be a ‘sham trust’.

Fatal error: Uncaught Error: Call to undefined function twentythirteen_paging_nav() in /home/clients/d17af2243e6f179e393695ba6e9ce04e/hsmnew/wp-content/themes/hsm/tag.php:33 Stack trace: #0 /home/clients/d17af2243e6f179e393695ba6e9ce04e/hsmnew/wp-includes/template-loader.php(78): include() #1 /home/clients/d17af2243e6f179e393695ba6e9ce04e/hsmnew/wp-blog-header.php(19): require_once('/home/clients/d...') #2 /home/clients/d17af2243e6f179e393695ba6e9ce04e/hsmnew/index.php(17): require('/home/clients/d...') #3 {main} thrown in /home/clients/d17af2243e6f179e393695ba6e9ce04e/hsmnew/wp-content/themes/hsm/tag.php on line 33